Omnichannel Banking Trends You Should Keep Tabs on in 2026

Updated on 6 Apr 2026

10 min.

Table of Contents

- Why omnichannel banking matters now?

- What omnichannel banking trends are shaping the year ahead?

- How is AI-powered personalization moving from batch to real-time decisioning?

- Why are voice and conversational banking becoming primary service channels?

- How does event-driven data replace batch ETL for cross-channel sync?

- How is proactive engagement shifting from campaign blasts to trigger-based journeys?

- Why are compliance automation and explainable AI becoming essential?

- How do financial wellness ecosystems drive contextual cross-sell?

- Why are branch and assisted channels resurging as advice hubs?

- How do you execute an omnichannel banking strategy?

- Where should you start: high-impact journeys or channel coverage?

- How do you unify customer data with a customer data platform and identity resolution?

- How do automated handoffs prevent repetitive support cycles?

- How do you operationalize AI with guardrails, not just models?

- How should you measure journey outcomes instead of channel metrics?

- How does Insider One help deliver omnichannel banking experiences?

- FAQs

Most Popular

Omnichannel banking in the year ahead focuses on connecting channels through shared data and decisioning. It unifies the data and decisioning behind channels so context travels with the customer. Most banks already offer mobile apps, web portals, branches, and call centers. What they lack is the orchestration layer that connects these touchpoints into a single, continuous experience. Most banks believe omnichannel is a channel problem. It’s not! It’s a decisioning and data orchestration problem.

This article breaks down omnichannel banking trends shaping how leading institutions allocate engineering resources and capital, and shows you how to execute an omnichannel strategy that delivers measurable lift without stalling on infrastructure complexity.

What should you know about omnichannel banking?

Omnichannel banking is about unifying the data and decisioning behind your channels, not just being present on all of them.

- Real-time artificial intelligence (AI) decisioning is replacing overnight batch processing for personalization

- Without a single customer view, you can’t execute any of this

- Most banks have the channels but lack the orchestration layer to connect them

Why omnichannel banking matters now?

Consider this example: a customer starts a mortgage application on their phone during lunch. They get stuck on a document upload and call the branch for help. The agent asks them to verify their identity, explain what they’re trying to do, and repeat information they already entered. The branch system has no record of the mobile session.

That’s what a fragmented banking experience looks like. And it’s expensive.

Omnichannel banking is different from multichannel banking in a critical way. Multichannel means you offer access via app, web, branch, and ATM. Omnichannel means those touchpoints share data, so context travels with the customer.

Banks that get this right see improvements in First Contact Resolution because agents have the full history immediately. They see lower Customer Effort Scores because customers don’t repeat themselves. And they see higher cross-sell conversion because offers reflect the total relationship, not just single-channel behavior.

What omnichannel banking trends are shaping the year ahead?

These aren’t predictions. They’re patterns already visible in how leading banks are allocating engineering resources and capital.

How is AI-powered personalization moving from batch to real-time decisioning?

Most banks still run AI personalization on segments updated overnight. A customer deposits a large sum in the afternoon, but the savings offer doesn’t appear until tomorrow’s batch runs. By then, the moment has passed.

The shift is toward real-time next-best-action decisioning. This means evaluating propensity, eligibility, and compliance at the exact moment of interaction. A decisioning layer combines machine learning scores with business rules:

- Propensity: How likely is this customer to accept?

- Eligibility: Do they meet product criteria?

- Constraints: Are there frequency caps or compliance blocks?

Real-time decisioning requires event-driven data infrastructure to update offers and service context during active customer sessions. Banks still running batch-only pipelines should sequence data modernization first. If you want to see what real-time decisioning looks like when it’s wired into journeys, book a demo.

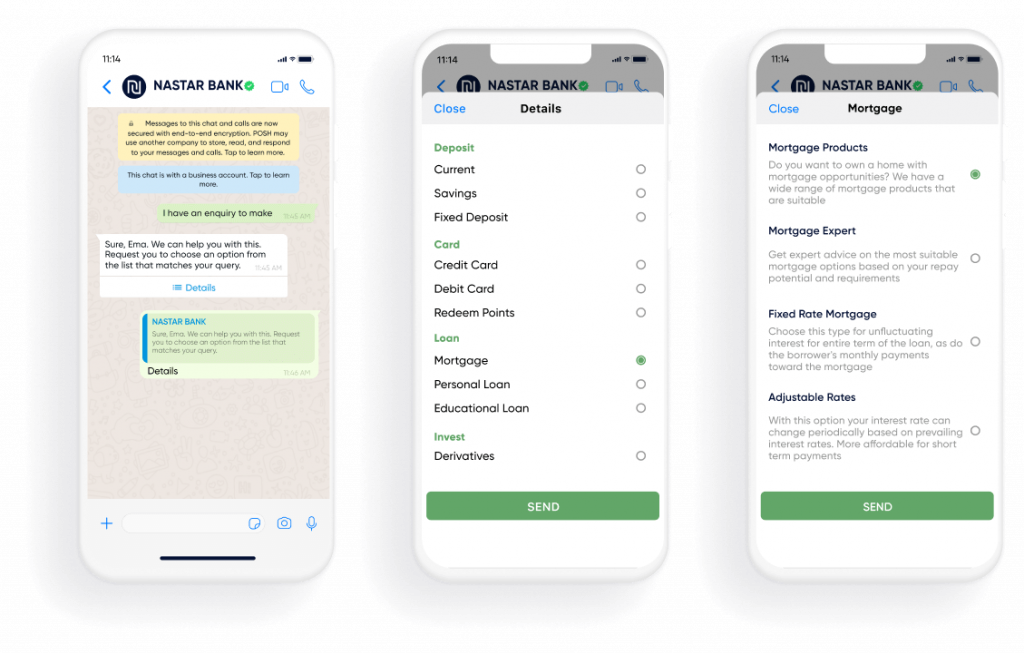

Why are voice and conversational banking becoming primary service channels?

Customers expect to resolve banking tasks through voice assistants and chat without visiting a branch or calling a support line. The metric that matters here is containment rate, the percentage of queries resolved without human escalation.

Banks often target higher containment for routine queries while ensuring escalation paths preserve context when a human agent takes over. When a bot hands off to a human, the agent should receive the full conversation transcript and customer intent. No re-authentication. No “can you tell me what you were trying to do?”

Security is non-negotiable. Voice biometrics and liveness checks help prevent spoofing, but they introduce friction. Finding the right balance depends on the risk profile of the transaction.

How does event-driven data replace batch ETL for cross-channel sync?

A customer updates their address in the app. The next day, they visit a branch and the agent sees the old address. This is the batch problem.

Event-driven architecture helps reduce these sync delays by propagating address changes as they happen. Instead of moving data in large chunks at scheduled intervals, changes propagate as individual events in near-real-time. Technologies such as Kafka and change data capture support this by moving updates between systems as individual events.

Event-driven infrastructure adds complexity around message ordering and ensuring events aren’t processed twice. But for banks with high volumes of digital transactions, it’s required for true omnichannel continuity. Smaller institutions with lower transaction volumes often do not need extremely low latency. If you want to assess what “event-driven enough” looks like for your stack, explore the patterns in our product demo hub.

How is proactive engagement shifting from campaign blasts to trigger-based journeys?

Traditional banking marketing pushes the same message to a broad segment at a scheduled time. Trigger-based engagement responds to individual behavior.

Effective triggers include:

- Salary deposit triggering a savings allocation suggestion

- Missed payment triggering a grace period notification

- Product expiration triggering a renewal offer

Without guardrails, this becomes spam. Fatigue caps limit messages per customer per week. Suppression rules block marketing to customers with open support tickets. And holdout groups let you measure incremental impact. Teams that launch triggers without holdouts can’t prove they’re working.

Why are compliance automation and explainable AI becoming essential?

Every personalized offer in banking must pass eligibility, suitability, and disclosure requirements. Historically, compliance reviews were manual bottlenecks. Many banks now embed compliance rules and audit trails directly into the decisioning layer to reduce manual review work.

Explainable AI (XAI) is the ability to show exactly why a specific offer was made to a specific customer. Audit processes often require teams to document why a model recommended a specific action. Customers expect it when they ask questions.

The regulations that matter: GLBA, GDPR, CCPA, CFPB rules on consumer data access, and the EU AI Act. Banks can reduce release friction by integrating compliance guardrails and audit trails into personalization workflows. If you want to see how teams operationalize that approach, book a demo.

How do financial wellness ecosystems drive contextual cross-sell?

Cross-sell used to mean showing the next product in a predetermined sequence. The modern approach triggers offers based on customer outcomes, not bank sales goals.

A wellness score aggregates signals like cash flow stability, savings rate, and credit utilization. When the score indicates a gap, the system triggers a contextual nudge. “You’re on track to hit your savings goal. Want to automate the last step?”

Suitability rules matter here. Offers must be appropriate for the customer’s financial situation, not just profitable for the bank. This is where compliance and personalization intersect.

Why are branch and assisted channels resurging as advice hubs?

Digital-first doesn’t mean branch-free. Branches increasingly support complex products such as mortgages, wealth management, and business banking. Routine transactions move fully digital.

The main challenge is maintaining continuity. A customer who starts a mortgage application online should arrive at the branch with their data pre-populated and their advisor briefed.

This requires appointment orchestration, a unified agent desktop showing digital history, and video banking as a hybrid option. The KPIs that matter: appointment conversion rate, handoff completion rate, and advisor utilization.

How do you execute an omnichannel banking strategy?

Most banks have the channels. What they lack is the connective tissue.

Where should you start: high-impact journeys or channel coverage?

Trying to unify all channels simultaneously is how initiatives stall. Pick a small number of high-impact journeys and build end-to-end continuity for those first.

Prioritize based on volume, revenue impact, and current friction:

- New account onboarding: High volume, high drop-off, sets the tone for the relationship

- Card dispute resolution: High support load, clear handoff points between digital and human

- Mortgage pre-qualification: High revenue, long consideration cycle, multiple touchpoints

Starting narrow means some journeys stay fragmented longer. That’s acceptable if the chosen journeys deliver measurable lift that funds the next phase.

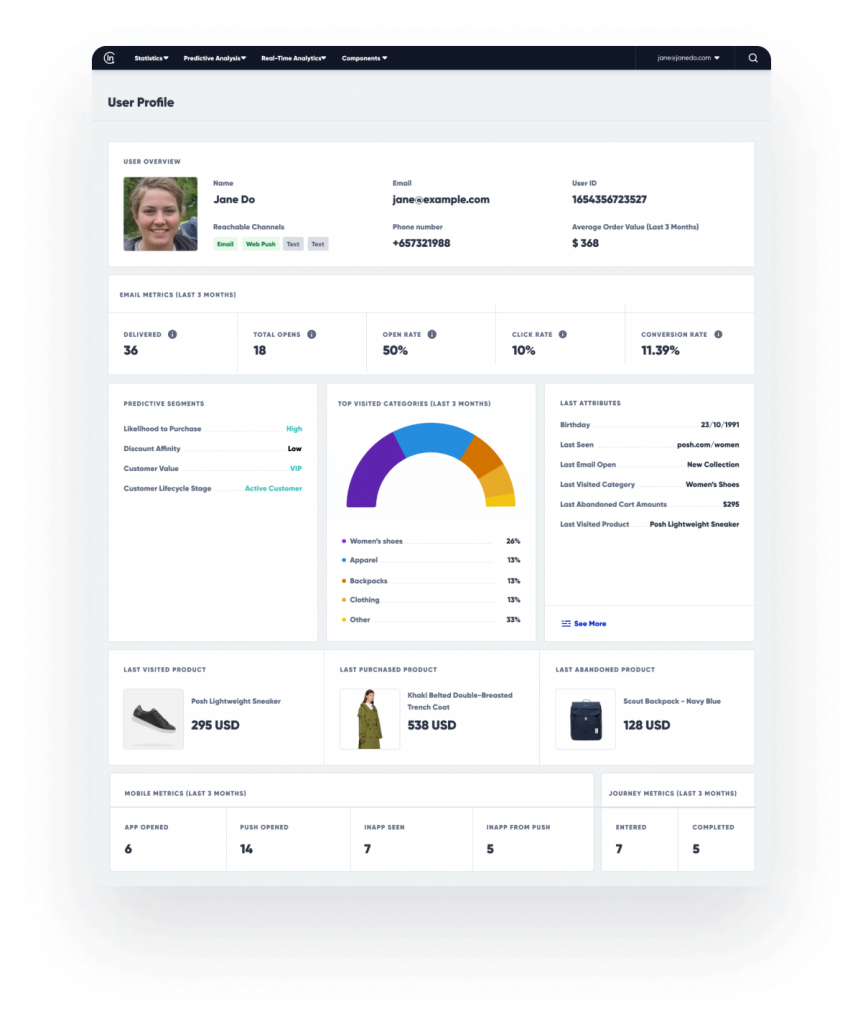

How do you unify customer data with a customer data platform and identity resolution?

Customer data typically lives in core banking, customer relationship management (CRM) systems, digital channels, and call center software. A customer data platform (CDP) collects and unifies this into a single profile, enabling real-time segmentation and activation.

Identity resolution is the process of matching records across systems using identifiers like email, phone, and account number. In banking, this is more complex than retail because you’re dealing with multiple products per customer, joint accounts, and business versus personal relationships.

For smaller institutions with a single core system, a well-integrated CRM may suffice. A CDP adds value when data is fragmented across multiple sources and real-time activation is required. If you want to see how unified profiles and identity resolution actually get activated across channels, head to the product demo hub.

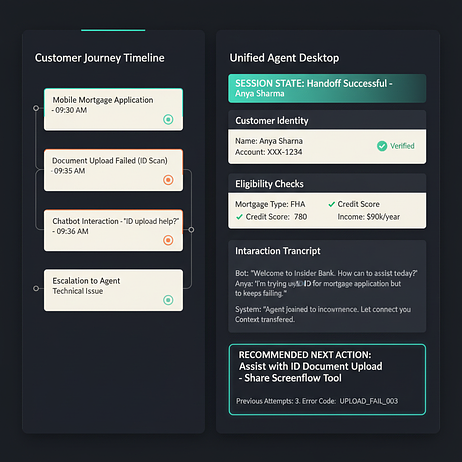

How do automated handoffs prevent repetitive support cycles?

A customer calls the contact center after starting a task in the app. The agent has no visibility into what happened. The customer re-explains everything. This creates a repetitive support cycle.

The fix is automated context handoff. When a customer switches channels, the receiving system inherits the session state: what they were doing, where they dropped off, what data they already provided.

Session state should be stored in the CDP or a shared context layer and surfaced to agents via a unified desktop. Teams often build handoffs for happy paths but forget edge cases, like when a customer abandons mid-authentication.

How do you operationalize AI with guardrails, not just models?

Deploying AI personalization without controls invites regulatory scrutiny. When you can’t explain why a customer received or didn’t receive an offer, you have a problem.

Operationalizing AI means wrapping models in explicit guardrails:

- Eligibility rules: Product-level constraints

- Suitability rules: Customer-level constraints like debt-to-income thresholds

- Frequency caps: Limits on offers per time period

- Decision trace: Audit log showing inputs, outputs, and final decision

Guardrails add latency. For high-risk products like credit, err toward more controls. For lower-risk engagement like content recommendations, lighter controls work.

How should you measure journey outcomes instead of channel metrics?

Most banks report channel metrics: app logins, call volume, branch visits. These don’t show whether the omnichannel experience is working.

- Onboarding: Time-to-first-transaction, document upload completion rate, drop-off by step

- Dispute resolution: Time-to-resolution, repeat contact rate, CSAT post-resolution

- Cross-sell: Offer acceptance rate, revenue per accepted offer, time from trigger to conversion

Journey-level measurement requires event-level data and cross-channel identity resolution. If that infrastructure isn’t in place, start with a single journey and instrument it fully before scaling.

How does Insider One help deliver omnichannel banking experiences?

Delivering omnichannel banking requires solving three foundational challenges:

- Fragmented customer data across systems

- Disconnected decisioning and personalization engines

- Channel-level execution without shared context

Most banks attempt to solve this by stitching together multiple tools – CDPs, campaign managers, analytics platforms, and AI engines. This creates latency, inconsistency, and operational overhead.

Insider One takes a different approach.

It unifies data, decisioning, and execution into a single platform so banks can deliver real-time, context-aware experiences without complex integrations.

Banks need a platform that unifies data, orchestrates journeys, and embeds AI with compliance controls, without stitching together separate tools.

- Unified Customer Database: Insider One consolidates data from core banking systems, digital channels, and third-party sources into real-time customer profiles with built-in identity resolution. This ensures that:

- Customer context is consistent across every channel

- Session history and behavioral signals are always up to date

- Personalization is based on the complete relationship – not fragmented data.

- AI-powered decisioning,The Insider One AI , Instead of running personalization in isolated systems, Insider One embeds AI-powered decisioning directly into customer journeys. This allows banks to evaluate in real-time:

- Propensity (likelihood to convert)

- Eligibility (product and regulatory constraints)

- Context (current session behavior and intent)

All decisions are governed by built-in guardrails, including:

- Frequency caps

- Suppression rules

- Suitability and compliance constraints

- Full decision trace for auditability

If you don’t have centralized, real-time decisioning, you don’t have true personalization -you have delayed targeting.

- Architect, Insider One’s customer journey orchestration solution: With Architect, Insider One’s journey orchestration layer, banks can design and automate end-to-end customer journeys across:

- Mobile and web

- Email, SMS, WhatsApp, and push

- Paid channels like Google and Meta

- Assisted channels including call centers and branches

Journeys are triggered by real-time events, not schedules—ensuring that engagement happens when it matters most.

- Conversational CX, Seamless handoffs between digital and human channels: Insider One enables context-aware channel transitions, so when a customer moves from app to call center or branch:

- Their session state is preserved

- Agents receive full interaction history

- Conversations continue without repetition

Most systems track interactions. Few systems transfer live context across channels. This is what enables true omnichannel continuity.

- Built for compliance, not retrofitted for it

In banking, personalization without compliance is not scalable. Insider One embeds:

- Audit trails for every decision

- Explainable AI for regulatory transparency

- Eligibility and suitability enforcement

- Consent and data governance controls

This ensures that every interaction is not only personalized—but also compliant by design.

Why this matters

Unlike traditional approaches that rely on stitching multiple systems together, Insider One provides a unified orchestration layer where data, decisioning, and execution operate together in real-time.

This reduces:

- Time to launch new journeys

- Operational complexity

- Dependency on engineering teams

And increases:

- Conversion rates

- Customer satisfaction

- Speed of innovation

If you’re done stitching point solutions together are are looking to move beyond fragmented multichannel experiences and build a truly connected, real-time omnichannel banking ecosystem, Insider One provides the foundation to make it happen. Book a demo before you dive into the FAQs.

FAQs

Omnichannel banking is a customer experience where interactions are continuous and contextual across all channels, including mobile app, web, branch, call center, and ATM. The key differentiator from multichannel is that customer context and session state persist across touchpoints.

Multichannel means the bank is present on multiple channels that operate independently. Omnichannel means those channels share customer context and session state so customers don’t have to repeat themselves when switching.

Core technologies include a CDP for unified profiles, event-driven data infrastructure for real-time sync, journey orchestration for cross-channel automation, and AI decisioning for personalization with compliance guardrails.

Key metrics include journey-level KPIs such as onboarding completion rate and time-to-resolution, customer experience metrics such as Customer Effort Score and First Contact Resolution, and channel handoff metrics such as context preservation rate and repeat contact rate.

Keep Reading

7 min.

Muharrem Derinkok

4 Jun 2026

11 min.

Chris Baldwin

2 Jun 2026

4 min.

Chris Baldwin

3 Feb 2026